EI Portfolio Performance History

As I look ahead to 2025, economic uncertainty in the US and China will be key drivers of commodity markets, particularly precious metals. While rising US interest rates could challenge gold and silver prices, geopolitical instability may increase demand from central banks and retail buyers, especially in China and Europe. I also expect more M&A activity in the precious metals space, with companies focusing on stable jurisdictions as risks grow in regions like West Africa.

In my portfolio, I’ve positioned for these trends by including high-grade gold and silver projects in stable regions, along with companies advancing critical minerals like copper, antimony, and rare earth elements. Several holdings are well-funded by major partners, while others are led by top technical teams exploring geologically promising districts. I’ve also included royalty companies with diverse portfolios and strong revenue growth potential, though some carry debt and geopolitical risks. The shift from green energy to security minerals, and the potential US deregulation to streamline permitting, offer new opportunities, and I believe my portfolio is well-prepared to navigate these challenges and capitalize on emerging trends this year.

Below, you will find a detailed breakdown of the portfolio's performance since its inception in 2008.

For in-depth analysis and access to my portfolio, including companies I track and evaluate to help you make informed investment decisions in the junior mining market, subscribe to my weekly newsletter today.

Good luck with your investments in 2025,

Joe Mazumdar

-

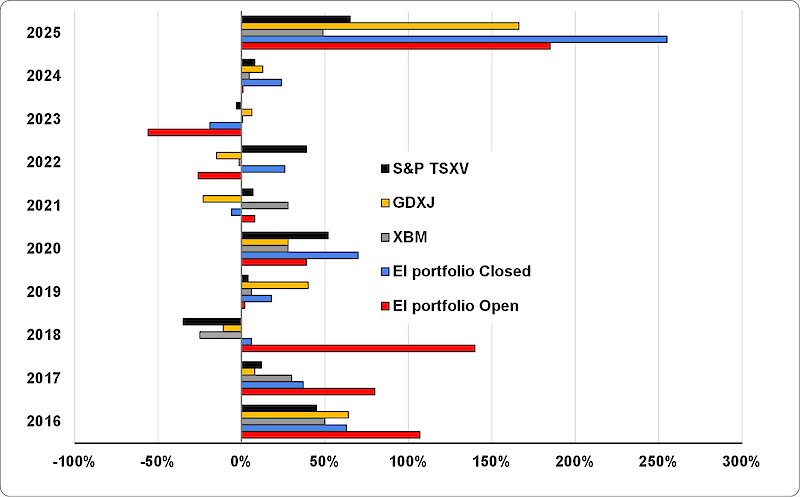

In 2025, the 19 companies within the current portfolio achieved an average return of 185%. Performance was led by a US-based critical mineral explorer/developer/producer, which benefited from operational advancements and a major transaction. Only one company — a grassroots precious-metal explorer in northern Europe — recorded a negative return for the year.

Regarding exits, 7 positions across 4 companies were sold in 2025, yielding an average realized return of 255%. These gains were primarily driven by the acquisition of a Top Pick cash-flowing royalty generator.

- Despite gold and silver being among the best-performing asset classes in 2024, the gold ETFs for major precious metal producers (GDXJ +13%, GDX +9%) did not deliver the expected leverage. By the end of the year, the portfolio comprised 19 companies, having closed out six positions and added four new ones. Most of the holdings were exposed to precious metals and copper. The 19 open positions delivered an average return of 24% and, since their initial inclusion, boasted an unrecognized return of 68%. In 2024, I exited six positions, which provided an average recognized gain of 1% despite the stocks' average annual drop of about 16%.

- In 2023, the benchmark resource equity ETFs for precious metals (GDXJ +6.3%), base metals (XBM +0.7%), uranium (URA +37.9%), and lithium (LIT -13.1%) displayed mixed results. However, the Exploration Insights portfolio, which was heavily weighted towards non-cash-flowing juniors, faced challenges. It underperformed the benchmarks on average with a decline of 19%, primarily influenced by grassroots, illiquid junior explorers, which experienced negative returns of 50-75%.

- At the outset of 2022, I anticipated a turbulent year for the markets predicated upon the exponential rise in COVID-19 infections due to the Omicron variant, higher-than-expected inflation rates, continued geopolitical conflicts, and climate change.

I was once again active, divesting myself of 11 positions in nine companies due to underwhelming results from drill programs, geopolitical risk, margin compression of precious metal producers, and better-managed companies. The average return from the closed positions was a disappointing -26%, roughly in line with the S&P TSXV Index performance (-39%), while the open position generated an unrecognized return of +26%.

- In 2021, I added 10 new positions while divesting 11 due to locking in some positive returns, an M&A transaction, and underwhelming drill results. Consequently, at the end of the year, the closed positions returned on average 8% while the open positions were down 6% versus the S&P TSXV Index which was up 7% over the same period.

- At the end of 2020, of the 23 miners in the portfolio (in 29 positions), 20 were listed in North America (TSX, TSX-V, and CSE) and three in the Australian Securities Exchange (ASX), providing exposure predominantly to precious metals (gold and silver) and less so to industrial metals (copper, nickel, palladium) and uranium.

The average unrecognized return from the open positions, which exceeded the benchmark by 25% on average, was 70%. I was active throughout the year, adding nine positions and selling 15 positions in 11 companies for an average recognized return of 39%. The S&P TSXV Index benchmark generated a robust 52% return over the same period.

- After making several adjustments in 2019, including closing 17 positions in 10 companies and adding seven new positions in new companies, the open positions comprised 30 holds in 20 companies. By the end of the year, the open positions had generated an unrecognized average return of 18%, and the overall return from the closed positions in 2019 was only 2% compared to a 4% return for the S&P TSXV Index.

- In 2018, I focused on the early side of the investment cycle due to the lack of exploration by major producers, especially in the gold sector. Most of our open positions were in prospect or royalty generators, while the remainder were in grassroots gold, copper, zinc, and lithium explorers, as well as gold developers, producers, or streamers. I was also active, adding 16 new positions —10 in new companies—and divesting seven positions in six companies. The sales or closed positions generated an average return of 140%, but the open positions only generated a 6% unrealized return, while the S&P TSXV Index benchmark yielded a return of -35%.

- In 2017, I saw a need to move down the food chain into earlier-stage projects that could develop into significant discoveries. This approach meant higher-risk, higher-reward plays that required careful analysis of exploration results and a commitment to cut bait quickly if results failed to meet our investment thesis. By consistently applying this process, I planned to continue reaping returns that exceeded the benchmarks.

I was pretty active, closing 18 positions via 22 transactions and opening 12 positions in 9 new companies, including two cash-flowing gold companies (producer and streamer), six explorers seeking gold, copper, zinc, and lithium, and four prospect generators focused on precious and base metals in the Americas. Positions closed in 2017 translated into an average weighted return of 80%, while the open positions generated an unrecognized return of 37% versus the S&P TSXV Index benchmark, which was up 12% over the same period.

- I joined Exploration Insights at the end of 2015 and took charge of the portfolio. Brent believed 2016 would be the year to actively buy the few high-quality deposits, mines, and management teams available, and I was eager to try.

The strategy paid off: Before the end of the year, I added three mid-tier gold producers and a couple of explorers. By December 2016, I had actively recycled the portfolio, closing 23 positions while adding 20 new ones, resulting in 24 open positions. The open positions provided us with an average return of 63%, while the realized gain for our closed positions was 107%.

I also started using the S&P TSX Venture (S&P TSXV Index) as a benchmark, as most of the stocks in my portfolio are listed on that exchange. The benchmark was up 45% in 2016.

- 2015 was a dismal year for miners, metals, and nearly all commodities and major markets. The Bloomberg Commodity Index was off 26%, metal demand was down 5.1%, and base metal prices were off 25% to 30%. The precious metal indexes were also down (HUI -32%, GDXJ -20%) while the TSX Venture Exchange hit an all-time low. The Exploration Insights portfolio finally succumbed to the bear market, showing an unweighted loss of 6%. In November, our cautious strategy turned more aggressive towards gold producers and explorers to position ourselves for the future by owning solid companies and assets rather than betting on a rising tide.

- In 2014, mining and metals were down again, with the Gold Bug Index (HUI) off ~18% (~38% from the 2014 high) and the S&P/TSX Global Mining Index (TXGM) down ~15% on the year (~26% from 2014 high). The GDXJ also had another bad year: off ~25% and down ~45% from its July peak. Worse still, the GDXJ fell a remarkable 86% from its high set in early 2011. The unweighted performance of the Exploration Insights portfolio for 2014 was a positive 18%. The strong performance reflected the sale of a few companies that had made metal discoveries before 2014 and the discipline to sell companies when results did not meet the investment theses.

- In 2011, the mining sector, particularly the junior sector as measured by the S&P TSX Venture Index (S&P TSXV), began to collapse, falling 26% in 2011, 23% in 2012, and 59% in 2013. By comparison, the Exploration Insights portfolio lost 2% in 2011, was down 14% in 2012, and off 18% in 2013.

- From its inception under Brent Cook's leadership in February 2008 through year-end 2010—including the Global Financial Crisis and the continuation of the Commodity Super Cycle—the Exploration Insights portfolio’s performance was strong. It returned an average 173% gain on sold positions and 319% on positions held at year-end.

![]() Sign up for our mailing list to receive the free Speculator's Checklist for Investing in Junior Mining report right away. Occasionally, we will also send you emails with links to interviews, articles, and more.

Sign up for our mailing list to receive the free Speculator's Checklist for Investing in Junior Mining report right away. Occasionally, we will also send you emails with links to interviews, articles, and more.

We will never rent, sell or give away your email address to anyone for any reason.